Three jobs that might grow more than expected in the age of AI

Maybe robots won't take all of our jobs after all?

When imagining powerful future technologies, it’s common to envision scenarios that put many people out of work. In this very newsletter, we’ve covered both an over-simplified aggressive prediction of arriving at a 15-hour average workweek by 2058, and an in-depth look at three jobs that will be seriously impacted by the current and next generation of AI.

But technology creates new jobs too. This isn’t always a 1-to-1 relationship— sometimes jobs are destroyed more quickly than they are created. But how might this play out over the next 10 years?

The Bureau of Labor Statistics (BLS) publishes a list of the fastest growing jobs, but their projections have historically been conservative, particularly in under-predicting the fast growing jobs of the 2010s like data scientists. Here are three jobs that might surprise us over the coming decade:

Biologists and medical scientists

Ever since the success of the Human Genome Project in the 1990s, it has been said that if the 20th century belonged to physics, the 21st belonged to biology. The extraordinary drop in the cost of genome sequencing over the past few decades has facilitated many discoveries from better understanding genetic illness to the use of CRISPR to edit the genes responsible. And given AI’s ability to quickly synthesize information and be employed in new types of experiments (plus impressive complementary advances in augmented reality), increasingly complex problems in the fields of neuroscience as well as biology and health in general could soon be solved.

From the perspective of the job market, the number of life scientists1 also surpassed the number of physical scientists in the 90s, and this trend keeps on continuing.

However, the BLS only projects a little over 30,000 new jobs in this field by 2033. That’s a lot less than the 77,000 that were added in the previous 9 years. While higher interest rates have put a damper on hiring since 2023, job announcements in scientific research are down about 12% relative to pre-pandemic, and the government funding that is responsible for about a third of overall R&D spending in life sciences is subject to change, it would be quite surprising (especially to the increasing number of grad students) to see such a slowdown persist for a whole decade when new technologies appear to be quickly expanding research possibilities.

The forecast

A more reasonable forecast should weigh the political and economic constraints of today against recent Nobel Prize-winning discoveries such as AI-enhanced protein design, and the greatly increased rate of discoveries in materials science. Innovations like these may over time compensate for the more uncertain political and economic environment. It’s also worth noting that life scientists are only a little more than 5% of overall pharmaceutical industry employment, so further efficiencies in other areas such as administrative work and new approaches to clinical trials might result in more resources being allocated to science, and at the very least allow the growth trend from the 2010s to continue. That would mean somewhere between 80,000 and 100,000 more biologists and medical scientists, roughly triple the BLS’ official forecast.

Counselors and therapists

With mental health taking a turn for the worse in the 2020s, along with even more people seeking treatment, one of the top 20 fastest-growing jobs are therapists, or as the BLS more specifically calls them, “Substance abuse, behavioral disorder, and mental health counselors”.

They predict about 19% growth by 2033— somewhat faster than the wider occupation of counselors2 at 12%, and much faster than the 3% growth predicted for the whole U.S. economy.

While this is 124,000 new jobs, such growth would still be a slowdown from the mental health crisis and the explosion of telehealth options that accompanied the pandemic. And yet jobs in the social assistance industry have returned to their longstanding trend of roughly 5% growth per year— almost 3x as fast as the 1.8% annual growth that the BLS predicts. Looking further forward, job postings in the community and social service sector tell a similar story. Google search trends for “mental health”, “therapist”, and “anxiety” remain high.

Estimating how much unmet need still exists explains why there is still so much growth. In 2022, 13% of American adults— nearly 33 million— reported seeing a mental health counselor. But this is still significantly less than the 23.1% who reported experiencing any mental illness that year. Cost and the difficulty of finding a provider are the most significant barriers even as salaries for counselors are low relative to the many years of education typically required. Low Medicaid reimbursement rates in some states, as well as strict degree requirements for Medicare reimbursements are a significant contributor to this problem, as these plans cover roughly 40% of Americans3. However, recent policy changes have expanded the range of counseling that Medicare plans are able to provide.

Future changes in government policies are hard to predict, but the complexity of finding a provider is a wicked problem that better tech still has some potential to solve. The process of finding the right professional for one’s unique circumstances in life can be an arduous one, especially for someone already struggling with mental health issues. And while ChatGPT may be a convenient option that a growing number of people are interested in (and which 80% of those who have tried have found effective), such tools might complement rather than substitute the human connection that is typically needed for recovery. But there are a few other complementary factors that might help expand access to counseling:

AI could bring down the software development and administrative costs for providers while enhancing the patient experience

A second wave of mental health tech might build on the lessons learned from the first one, including incorporating more clinician feedback into the wide variety of tools that exist

Better information sharing across disciplines might result in more targeted, effective, and economical therapy options that open the door to more patients

Insurance companies, instead of trying to avoid paying providers, might recognize the connection between mental and physical health and prioritize getting more patients the preventative mental healthcare they need so as to avoid more expensive physical ailments

More people from under-represented-in-counseling backgrounds (in particular men, who are less likely to report seeking care) could enter the field

At least some of these factors are likely to support continued job growth in counseling. And beyond just addressing the current deficiencies, there is a real possibility of quality improvements as well. While 85% of Americans who have sought out counseling have found it at least somewhat effective, there are a number of new technologies and initiatives in development that might further support the mental health professionals of the future. Perhaps we’ll one day look back on the 2020s epidemic of mental illness as we now look at cholera outbreaks— something that came with a particular stage of modernization, but as its source became better understood, became increasingly manageable and preventable over time.

Some good news (for both counselors and the public in general)

There is evidence of a real improvement in mental health so far in 20244, whether due to effective counseling, the shock of social media on well-being5 wearing off, or even the possible addiction-reducing properties of Ozempic. That we saw more demand for counseling in 2024 even as overall mental health appeared to improve suggests that a shift in culture might drive growth in this area going forward. There is a big disparity in the prevalence of mental health issues across age groups, and over 50% of Gen Z having received professional mental health services at some point. With therapy of this nature so normalized, it wouldn’t be surprising to see increases not only in mental health counseling but also in marriage, career and other forms of counseling, especially if technology accelerates changes in daily life. With this in mind, it’s also worth noting that worries about the future are the #1 source of anxiety for Gen Z— and worries about finances are not far behind. This is all the more reason to work on more accurate job forecasts!

The forecast

Taking all of this together, it seems like 3% annual average growth over the next 10 years seems like a nice middle-of-the-road estimate between a continuation of current trends and the possibility that better technology or circumstances might reduce the need for counseling. That’s a 34% total increase, or 230,000 more jobs than the official forecast!

23,000 new jobs per year is slightly more than the latest graduation rates of counseling programs. But enrollment could increase in the future, or the demand could be filled by a mix of professionals from other fields like psychiatric nurse practitioners or in industries where educational requirements might be loosening such as religious6 and nonprofit social service organizations7. The strong connection between exercise and mental health might also open up new avenues of treatment.

A 34% increase in mental health counselors might mean going from 13% of Americans regularly seeing a professional to over 17%8 — much closer to current needs and possibly even fully meeting them if rates of mental illness continue to fall. By the 2030s, some of the more complex problems in neuroscience mentioned above may have also been solved, further contributing to “cognitive freedom”. In such a world, the human element of counseling may evolve with the increased number of possibilities, but I predict that it will still be just as important.

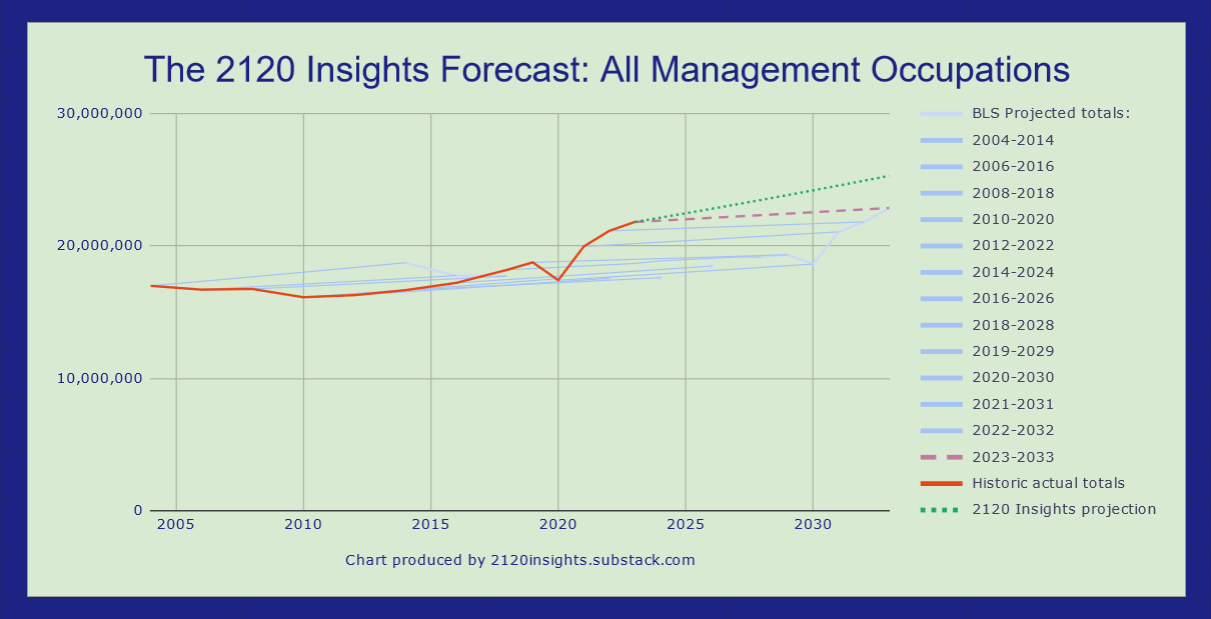

Management

Researchers in the field of AI safety often speak of the “alignment problem”: given sufficiently intelligent AI, how will we ensure it can still help us produce the things that we value?

While there will be many technical details to work out in the years to come as AI systems are designed to operate computers and integrate more deeply into workflows, a big part of the solution might be an old school one— more empowered managers.

Even in fields like software development that started seeing a slowdown in hiring in 2022 and AI-enhanced productivity since then, the growth in managers has been robust.

This makes sense, for a variety of reasons. Where new technology improves productivity, prices usually fall, and more complex products and services can become affordable. But as production processes change and/or the scope of work expands, the complexity of decisions that managers need to make can also increase.

Now, this may be less true in fields where the products or services produced are simple and unlikely to change much. But earlier waves of automation in agriculture and manufacturing have left relatively few jobs in these industries. In fields from science to logistics to construction, one can imagine how complementary intelligent systems (including increasingly capable robots) could further increase the complexity of what is produced and require more management decisions, including when to deploy artificial vs. human intelligence. There is already research to show how managers are often more effective users of AI than younger “AI natives”.

A counterpoint to this is where AI has been employed in automated reporting up to leadership, cutting out layers of middle management. But here, I think it is helpful to draw a distinction between managers and supervisors. Where the number of human individual contributors shrinks, the number of first-line supervisors likely will as well. But just as some have hypothesized that AI tools might empower more “solopreneurs”, greatly assisting them with sales and customer service functions, an increasing number of individual contributors in larger organizations might oversee enough automated and hybrid processes to be considered managers as well, albeit with fewer human direct reports.

A helpful way of seeing how this trend is evolving over time is by looking at the ratio between managers and line level employees across different fields (as reported by BLS):

The ratio of managers in sales, marketing, advertising, and public relations relative to other sales workers, and how much it’s grown— up 50% since 2016(!) is quite striking. While part of this story is the 2010s decline in retail, the number of managers has actually been rising even faster. It’s also worth noting that marketing and public relations teams have some of the highest rates of AI adoption. The departments that are making the heaviest use of AI could end up becoming the more influential ones in their companies.

Supporting the theory of increasingly complex work requiring more managers, we also see a notable rise in the ratio of managers to line-level employees in science and tech. But suppose we invert this chart to show how many line-level employees there are per manager, and also include BLS 2033 projections?

The number of employees per manager is quickly falling in many sectors—administrative services and transportation, storage, and distribution are the most noticeable ones, but we see a significant drop in this ratio in the fields of industrial production and medical/health services too. Surprisingly, the BLS doesn’t forecast any further change in this ratio across most fields; this is another area where I suspect these projections could be improved. A future where AI has advanced considerably could see the number of employees per manager in some fields fall to near one, as it is in agriculture.

Among the sectors where the ratio of employees per manager is falling the quickest, circumstances vary quite a bit. In administrative services, which includes customer service and secretarial work, it’s because the number of line employees is falling significantly, but the number of managers is increasing slightly. In transportation and distribution, it’s because growth in management has outpaced even the unexpected increase in warehouse workers. As robots in warehouses become more sophisticated, we might expect to see more line level-employees shift into management.

Looking at charts like the one above, it seems like the collapse in the employee-to-manager ratio is just getting started. At the very least, I think we can expect to see 1.5% growth per year— similar to the trend since 2018, but taking into account slower growth in the labor force overall. That would be roughly 3.5 million more jobs by 2033.

The bottom line

Between ~70,000 more life scientists, 230,000 more counselors, and 3.5 million more managers, we’re looking at 3.8 million more jobs overall! This is substantially more than the 2-3 million additional jobs we might expect to lose due to technological displacement from telemarketers, customer service reps, and administrative assistants. However, we need to be careful here. Most of these new jobs require either extensive education or experience which won’t be as easy for laid off workers from other fields to pick up. Even more importantly, the growth in managers may come mostly from promotions and reclassifications, meaning effective declines in other occupations. So it is still highly possible that we lose jobs on net.

The circumstances here are consistent with something I’ve observed before: the job market might continue to be relatively decent for experienced workers, but increasingly tough for young people, especially if updates to school curricula lag behind the knowledge and skills needed to be successful in increasingly AI-augmented disciplines. While unemployment has ticked up a bit in 2024, it is noticeably worse for those under 25— a problem that newly-elected governments both at the federal and state/local level will have to keep a close eye on.

“Learning to code” was common advice for young people and career switchers alike in the 2010s. But is it such good advice today? Or is it better to learn a trade?

Over the coming weeks, I’ll answer these questions while taking a look at a few sectors where job prospects are a little more uncertain and could swing the economy one way or the other.

By “Life Scientists” I am specifically referring to all of the following occupations together:

Animal Scientists (19-1011)

Food Scientists and Technologists (19-1012)

Soil and Plant Scientists (19-1013)

Biochemists and Biophysicists (19-1021)

Microbiologists (19-1022)

Zoologists and Wildlife Biologists (19-1023)

Biological Scientists, All Other (19-1029)

Conservation Scientists (19-1031)

Foresters (19-1032)

Epidemiologists (19-1041)

Medical Scientists, Except Epidemiologists (19-1042)

Life Scientists, All Other (19-1099)

Growth prospects appear to be the strongest for Medical Scientists, Except Epidemiologists and Biological Scientists, All Other

The wider occupation of counselors includes the following:

Career Counselors (21-1012)

Marriage and Family Therapists (21-1013)

Rehabilitation Counselors (21-1015)

Substance Abuse, Behavioral Disorder, and Mental Health Counselors (21-1018)

Counselors, All Other (21-1019)

Medicare and Medicaid paid for about 45% of total mental health care spending in 2019.

SAMHSA’s National Survey on Drug Use and Health (NSDUH) shows a that the percent of Americans reporting any mental illness dropped from 23.1 to 22.8 from 2022 to 2023. National Health Interview Survey (NHIS) data even show that there were fewer people suffering daily from depression in 2023 than there were in 2019 (though there were more people suffering from it on a weekly or monthly basis). But even more remarkable is the decline in both anxiety and depression reported in the Census’ Household Pulse Survey. Throughout 2023, this rate ranged from 28.8 to 34.2, but starting in 2024, it has been between 20.5 and 21.4!

Such a big drop is likely due to a methodological change, possibly to bring reported rates of mental illness in closer alignment with NSDUH and NHIS data as the Pulse Survey evolves into the Household Trends and Outlook Pulse Survey (HTOPS). Even so, if these results predict another 1-2% drop in reported mental illness in the 2024 NSDUH, they will be quite a useful barometer that we can check in on every other month.

This is a hotly contested topic, with some papers arguing that the impact of social media doesn’t show up in overall international surveys of well-being. However, this review of the literature (also linked above) makes a strong case for social media use impacting individuals very differently— some benefiting considerably while others see an increase in anxiety and depression that cancels out the benefit.

If it is true that social media had a greater negative impact on a particular group within the population, it seems possible to realize significant improvement by targeting interventions to this group specifically.

The relationship between religion, spirituality, and mental health is a complex one. While earlier schools of thought put more distance between psychiatry and religion, a survey of recent literature suggests religiosity reduces the likelihood of depression by about 16%. However, American religiosity continues to fall, particularly among younger generations who are most affected by the decline in mental health. There may be some opportunities for religious providers to try new approaches and cast a wider net given the need.

That said, it’s notable that while membership in churches/synagogues has declined from 70% to 45% from 1992 to 2023, actual reported attendance fell only from 40% to 32%. This suggests that the remaining members are more devout than they were a generation ago, making the gap between traditionally religious and non-religious people wider than ever. If we see improvement in mental health over the coming decade, will it reduce the gap in mental illness between the religious and non-religious? Or will a religion (old or new) arise to successfully meet the need?

A more detailed breakdown of Substance abuse, behavioral disorder, and mental health counselors shows a strong increase in employment across all major industries. Below is the 10-year moving average of annual growth of each industry that employed a significant number of counselors, including the latest BLS 2023-2033 projection:

It seems unlikely that the growth rate would fall so significantly in every industry. Averaging 3% per year through 2033 seems like a much more reasonable (and even conservative) assumption.

There is also the possibility that existing patients might have more regular appointments. Based on NHIS data reported by this KFF report and BLS employment estimates, there was only one counselor for every 84 people who reported seeking counseling in 2022— enough for about one per individual appointment per month. While many people stop going to therapy after just one appointment, studies show it often takes at least 2-6 months of regular appointments to resolve issues.

I feel a bit cautious about the counsellor forecast because anecdotally and in surveys, therapy seems to be one of the most popular uses of AI at the minute.

Mostly this seems to be new demand – people are speaking to their AI therapist every day and then also speaking to a human therapist once a week, or are using AI therapy when they wouldn't have bothered to get a human therapist before. And I think people could do 10x more therapy than they do today.

So I don't expect an immediate impact on employment.

But AI therapy seems like seems likely to continue to improve as models get better memory of past interactions, plus better social skills as they get larger (e.g. GPT-4.5 vs 4), more personality (maybe realistic video avatars). In combination with advantages like unlimited free 24/7 availability, infinite patience and ability to provide any therapy style, it wouldn't be surprising if people stopped bothering to see their human therapist.